Partners

Countries at all income levels have the opportunity to build lasting economic growth and at the same time reduce the immense risk of climate change. But action is needed now.

The Global Commission, advised by some of the world’s leading economists, sets out a ten point Global Action Plan for governments and businesses to secure better growth in a low-carbon economy.

We live in a moment of great opportunity, and great risk.

The opportunity is to harness the expanding capacities of human intelligence and technological progress to improve the lives of the majority of the world’s people. Over the last quarter of a century, economic growth, new technologies, and global patterns of production and trade have transformed our economies and societies. In developing countries, nearly 500 million people have risen out of poverty just in the last decade – the fastest pace of poverty reduction for which we have data. 1 But still 2.4 billion live on less than US$2 a day, and urbanisation, rising consumption and population growth have put immense pressure on natural resources.

The next 10–15 years could be an era of great progress and growth. 2 In this period we have the technological, financial and human resources to raise living standards across the world. Good policies that support investment and innovation can further reduce poverty and hunger, make fast-growing cities economically vibrant and socially inclusive, and restore and protect the world’s natural environments.

But such a positive future is not guaranteed. Indeed, from the perspective of many economic decision-makers today, the outlook is troubling. Since the financial crash of 2008 and the recession that followed it, many countries have been struggling to achieve sustained prosperity. Job creation and productivity growth are widely inadequate, and inequality is rising in many places. Many low-income countries no longer know if they will be able to replicate the successes of middle-income countries. 3 Extreme poverty, low employment levels, and poor health and education outcomes are persistent problems.

Many emerging economies also fear getting stuck in an outdated model of economic development. It is striking that of over 100 countries labelled “middle-income” half a century ago, only 13 have since achieved high-income status. 4 Many have found it difficult to pursue sufficient investment in public services to meet the expectations of their rapidly expanding middle classes. Air pollution has also emerged as a major economic and social cost, with outdoor pollution alone linked to nearly 4 million premature deaths per year. 5

Meanwhile, most high-income countries are struggling with weak, unevenly distributed economic growth. Fragile public finances and continuing high levels of public and private debt are compounded by anxieties over competitiveness, inadequate investment in infrastructure renewal, and the pressure of ageing populations. 6

Then there are the unprecedented risks posed by climate change. The strong growth of the global economy before the financial crisis was accompanied by a marked surge in greenhouse gas (GHG) emissions. 7 Most of this came from the growing use of fossil fuels, along with other sources including agriculture, deforestation and industry. If current emission trends continue unchecked, the resultant increase in average global temperature could exceed 4°C above pre-industrial levels by the end of the century. This would be more than double the 2°C rise that world leaders have set as a limit to avoid the most dangerous climate impacts. 8

The risks associated with such warming are very large. They range from an increase in the frequency of extreme weather events such as floods and droughts, to severe pressures on water resources, reductions in agricultural yields in key food-producing regions, and losses of ecosystems and species. Changes in seasonal weather and precipitation patterns are already being observed, which can greatly affect rural livelihoods. Some additional warming is unavoidable due to the greenhouse gases already in the atmosphere. 9 Climate risks increase disproportionately as temperatures rise, becoming particularly high above 3°C of warming, as irreversible “tipping points” may be reached such as the collapse of ice sheets and resulting sea-level rise. 10

It is very difficult to estimate the economic costs of such effects, as there are many uncertainties. But the Intergovernmental Panel on Climate Change (IPCC) suggests that the likely costs of just 2°C of global warming would be of the order of 0.5–2% of global GDP by the middle of the century, even if strong adaptation measures are taken. Once warming has proceeded beyond this, the costs will rise further – though the IPCC finds there is too much uncertainty to estimate reliably by how much. 11 What the IPCC does confirm is that climate change impacts will affect the world’s poorest people the most; they are already doing so. But countries at all income levels face serious climate risks, as recent studies of the United States (among others) have shown. 12

Effective adaptation will be crucial to tackle the effects of warming already built into the climatic system, but it is not enough. Without stronger mitigation efforts in the next 15 years, which lead global emissions to peak and then begin to decline, the risk of exceeding 2°C of warming will greatly increase. 13 Delay in managing climate risk only worsens the problem. It increases the concentration of greenhouse gases in the atmosphere and their warming effect. And it makes it harder and costlier to shift course later on, 14 as the stock of high-carbon assets – and the number of people whose wealth and livelihoods depend on them – keeps growing, and low-carbon research and development (R&D) continues to lag.

The time to tackle climate risk is therefore now. Yet climate change is rarely the top priority for those whose decisions most affect it. Most policy-makers and business leaders face more immediate issues and risks. Many have understandable concerns about actions or investments which, whatever their long-term benefits, could involve short-term costs or loss of competitiveness. And they face particular barriers to addressing a problem, such as climate change, that requires international cooperation. This is particularly true for those in developing countries, which have not been historically responsible for causing climate change, and which still face huge challenges in reducing poverty and raising living standards. They want to be sure that wealthier countries will do their fair share, and will provide adequate finance to support poor countries’ efforts.

The challenges for economic decision-makers are thus profound. Can they overcome current economic problems and establish new models of growth? Can they, simultaneously, act to reduce climate risks?

The evidence presented in this report shows the answer to both questions is “yes”. The structural and technological changes unfolding in the global economy, combined with multiple opportunities to improve economic efficiency, now make it possible to achieve both better growth and better climate outcomes. The purpose of this report is to help economic decision-makers, in both the public and private sectors, make the most of this opportunity – and do so now.

There is a perception that strong economic growth and climate action are not, in fact, compatible. Some people argue that action to tackle climate change will inevitably damage economic growth, so societies have to choose: grow and accept rising climate risk, or reduce climate risk but accept economic stagnation and continued under-development.

This view is based on a fundamental misunderstanding of the dynamics of today’s global economy. It is anchored in an implicit assumption that economies are unchanging and efficient, and future growth will largely be a linear continuation of past trends. Thus any shift towards a lower-carbon path would inevitably bring higher costs and slower growth.

But “business as usual” in this sense is an illusion. New pressures on resources, changing structures of global production and trade, demographic change and technological advances have already altered countries’ growth paths. They will make the future inescapably different from the past.

The reality is that under any circumstances the next 15 years will see major structural transformations in the global economy. As population growth and urbanisation continue, global output is likely to increase by half or more. 15 Rapid technological advances will continue to reshape production and consumption patterns. Total investment in the global economy is likely to be of the order of US$300–400 trillion. 16 Of this, around US$90 trillion is likely to be invested in infrastructure across the cities, land use and energy systems where emissions will be concentrated. The global scale and speed of this investment will be unprecedented: it will inevitably result not in incremental or marginal changes to the nature of economies, but in structural ones.

But what kind of structural changes occur depends on the path societies choose. There is not a single model of development or growth which must inevitably follow that of the past. These investments can reinforce the current high-carbon, resource-intensive economy, or they can lay the foundation for low-carbon growth. This would mean building more compact, connected, coordinated cities rather than continuing with unmanaged sprawl; restoring degraded land and making agriculture more productive rather than continuing deforestation; scaling up renewable energy sources rather than continued dependence on fossil fuels.

In this sense, the choice we face is not between “business as usual” and climate action, but between alternative pathways of growth: one that exacerbates climate risk, and another that reduces it. The evidence presented in this report suggests that the low-carbon growth path can lead to as much prosperity as the high-carbon one, especially when account is taken of its multiple other benefits: from greater energy security, to cleaner air and improved health.

This analysis rests on a considerable body of experience and research on the relationship between economic growth and development, and climate action. This includes academic literature as well as policy and business reports by the Organisation for Economic Co-operation and Development (OECD), United Nations agencies, multilateral development banks, the International Energy Agency (IEA) and many others. 17 The Commission’s work has drawn extensively from this body of applied economic learning, as well as from many interviews with economic decision-makers in governments, city and subnational authorities, and businesses, and with investors across the world.

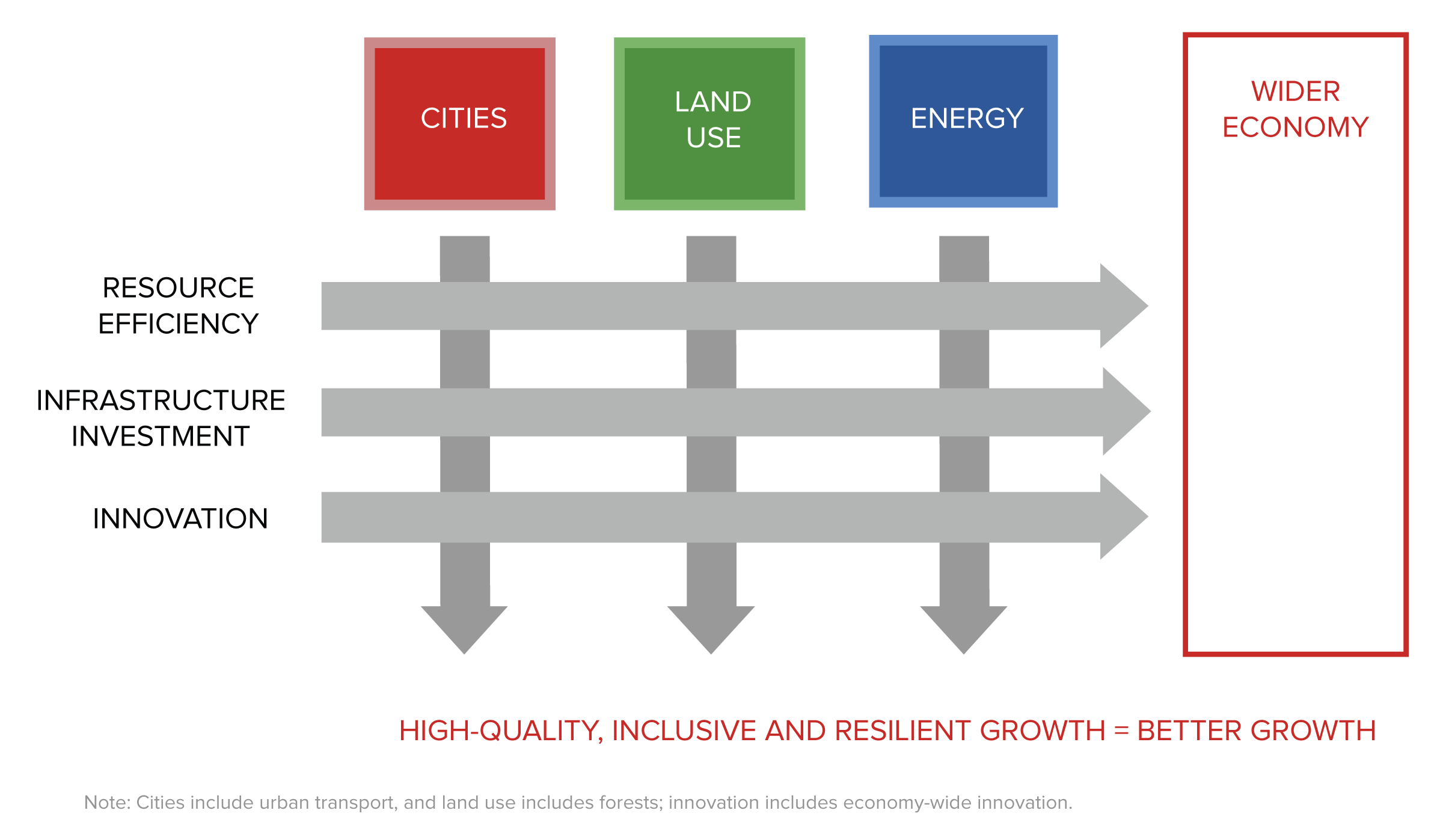

A central insight of this report is that many of the policy and institutional reforms needed to revitalise growth and improve well-being over the next 15 years, can also help reduce climate risk. In most economies, there are a range of market, government and policy failures that can be corrected, as well as new technologies, business models and other options that countries at various stages of development can use to improve economic performance and climate outcomes together. These opportunities exist in the short (less than 5 years), medium (5–15 years) and long term (greater than 15 years), as the various chapters of this report show. They require good policy design and implementation across three main drivers of change:

The report’s analysis focuses on three key economic systems which will be the locations of much of the growth in the global economy over the coming decades, and which are also the sources of most global GHG emissions. They are:

The large investments to be made in the next 15 years in these three systems make this a critical time for defining countries’ economic trajectories. Many of these investments will involve capital assets that last three to four decades or longer. They will thus play a key role in shaping the performance of the global economy not just in the next 15 years, but for the next half-century. The carbon-intensity of those investments, meanwhile, will largely determine the scale of future climate risk.

Note: Cities include urban transport, and land use includes forests; innovation includes economy-wide innovation.

The Commission’s work has focused on these three systems and on the drivers of change that are crucial to transforming them. But those drivers of change also have a broader role to play across the economy. For example, innovations in products and processes are already transforming the economic and emissions performance of energy-intensive process industries such as steel, aluminium, cement and chemicals, and will be central to future growth and emissions reduction. 31

Strengthening growth and tackling climate risk are therefore not just compatible goals; they can be made to reinforce each other. However, this will not happen automatically. It requires policy-makers to adopt an explicitly low-carbon pathway in economic policy. All three drivers need to be harnessed across all three economic systems. Above all, credible and consistent policy signals must be sent to businesses and investors.

This is essential: government-induced uncertainty is the enemy of investment, innovation and growth. The current vacillating and mixed signals on climate policy in many countries, especially in terms of a predictable carbon price, pose a significant dilemma for investors. In the long run, there is a significant risk that high-carbon investments may get stranded as climate policy is strengthened. But in the short run, many low-carbon investments are riskier and less profitable than they might be with strong climate policies. This uncertainty has raised the cost of capital and encouraged investors to hedge their bets between high- and low-carbon assets. Investment, jobs and growth all suffer as a result.

The conclusion that growth and climate goals can be mutually reinforcing is not surprising in the long run, beyond 15 years ahead. As the impacts of climate change grow larger, the potential harm to economies will increase. What this report shows, however, is that low-carbon policies can also generate strong growth in the medium term (5–15 years), provided that governments make the necessary policy and investment choices. Building more compact cities with good public transport, for example, not only reduces GHGs, but also allows people to move faster and more efficiently from home, to jobs, to shops and services; it reduces traffic congestion and air pollution, and it provides new business opportunities around transport hubs. Harnessing domestic renewable energy resources can boost energy security and reduce trade deficits. There is growing evidence that clean-tech R&D has particularly high spillover benefits, comparable to those from robotics, information technology (IT) and nanotechnologies.32

Even in the short term (the next five years), there are multiple opportunities to advance both economic and climate objectives by correcting market failures and policy distortions. No economy today is perfectly efficient, and many efforts to make key resources more affordable – such as by subsidising fossil fuels, water or fertilisers – have the unintended consequence of promoting inefficiency and waste. Policies to support established businesses may stifle competition from low-carbon innovators. Lack of coordination across levels of government and between neighbouring communities can lead to scattered development and sprawl, increasing the cost of infrastructure and public service delivery. Better policy design can correct these problems, increasing economic efficiency while lowering GHG emissions.

Of course, there are also many trade-offs. There are many immediate ways to achieve strong growth with higher emissions. Not all climate policies are “win-win”. The low-carbon transition will have winners and losers, and these costs will have to be faced and managed, as we discuss in more detail below. But short-term policies which weaken the prospects for stronger economic performance in the medium and long term also have real costs which should be properly acknowledged. Over time, growing climate change impacts will disrupt industry, farms and communities, with disproportionate harm to low-income countries and people, and require even greater government intervention. In such a context, it is unwise to be short-sighted.

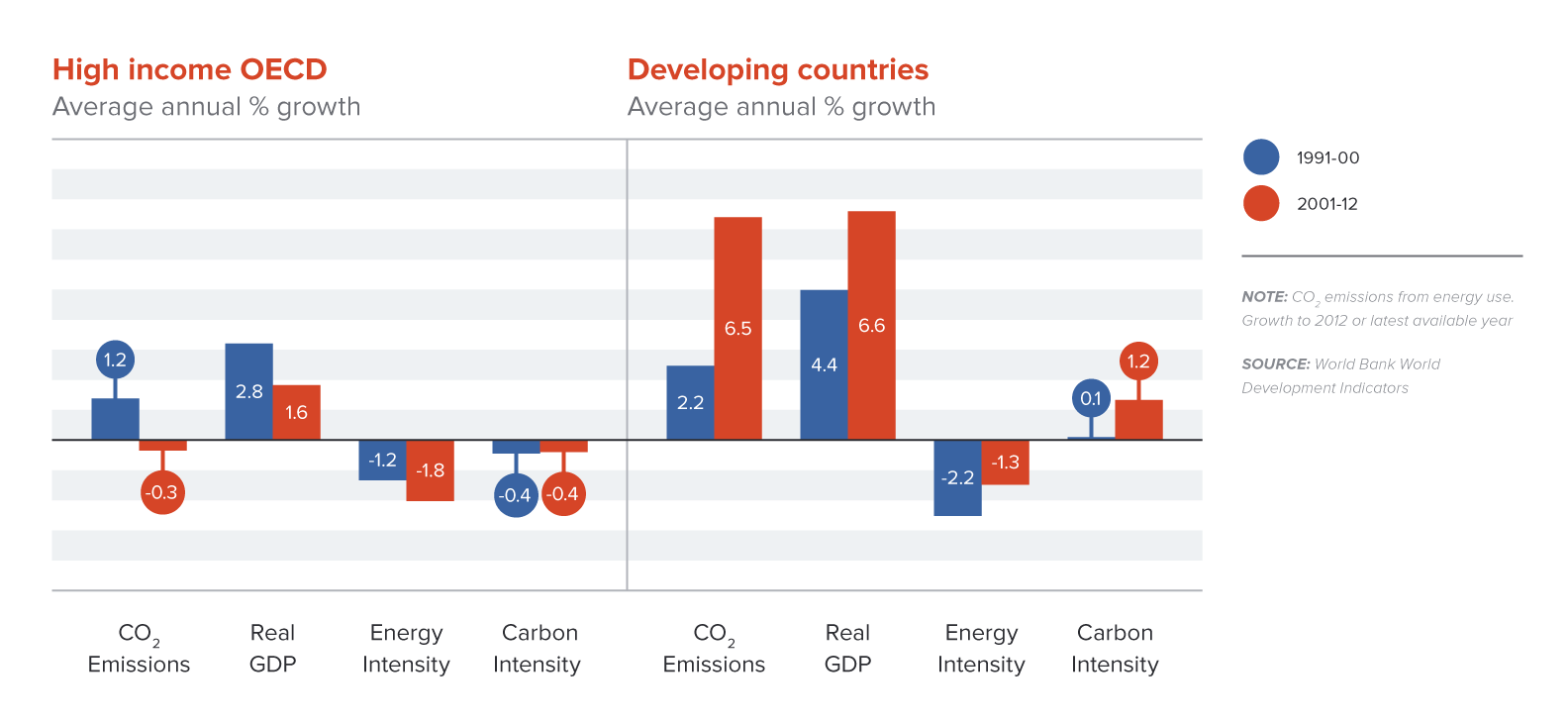

The evidence for these conclusions has been accumulating over the last decade. The theoretical basis for them has been known for some time. What is new is the practical experience around the world. National and local governments as well as businesses that have adopted lower-carbon strategies and policies have found them associated with economic performance as good as or better than their high-carbon peers’. 33 Much of this has been driven by recent technological advances. The decoupling of growth from carbon emissions in some of the best-performing economies, both in Northern Europe and in North America, demonstrates the gains that can be made in incomes, jobs, rates of innovation and profits from a low-carbon, resource-efficient model of growth. 34

Lower-carbon growth will look different in low-, middle- and high-income economies, and according to national circumstances. The Commission’s work has drawn on national studies in countries as diverse as Brazil, China, Ethiopia, India, the Republic of Korea and the United States. All exhibit multiple opportunities to achieve strong economic performance while reducing GHG emissions, but with very different policy, sectoral and investment mixes.

One question that arises from this analysis is whether lower-carbon forms of growth cost more than higher-carbon ones, in the sense of requiring greater capital expenditure. Analysis for the Commission shows that, in fact, the difference in infrastructure investment needs is likely to be relatively modest. As noted earlier, an estimated US$90 trillion will be invested in infrastructure in 2015–2030 (about US$6 trillion per year); a shift to low-carbon investments would add about US$4 trillion (about US$270 billion per year). 35 That would be less than a 5% increase in projected aggregate infrastructure investment requirements (see Figure 2).

The reason for this is that the higher capital costs of renewable energy and more energy-efficient buildings and transport systems would largely be offset by lower energy supply requirements due to energy efficiency savings, reduced fossil fuel investment, and the shift to better-planned, more compact cities. And there could be additional savings in operating costs once investments are in place – for example, from shifting to renewable energy sources and away from fossil fuels. These savings could potentially completely offset the additional capital investments. 36 Still, the costs will need to be financed, which for many developing countries will require international support. We discuss this further below.

Source: Climate Policy Institute and New Climate Economy analysis based on data from IEA, 2012, and OECD, 2006, 2012. 37

The transformational changes proposed in this report offer an opportunity not just to drive economic growth defined in terms of incomes and GDP, but to achieve multiple benefits, improving human well-being more widely. This underpins the Commission’s concept of “better growth”: growth that is inclusive (in the sense of distributing its rewards widely, particularly to the poorest); builds resilience; strengthens local communities and increases their economic freedom; improves the quality of life in a variety of ways, from local air quality to commuting times; and sustains the natural environment. All these benefits matter to people, but they are largely invisible in GDP, the most widely used measure of economic output.

In this sense the quality of growth matters as much as its rate. That means decision-makers need better tools to evaluate the impact of specific policies and actions, and to track economic performance more broadly. The Commission therefore supports the development and use of a wider set of economic indicators. If high rates of growth, for example, result in high levels of air pollution or environmental degradation, or if the rewards of growth are not widely distributed to reduce poverty and unemployment, it is legitimate to ask whether the economy is truly performing well. By the same token, if GDP growth is slower but other indicators show improvements, economic performance may be regarded as superior. These are judgements which people and governments will make in their own ways. 38

History suggests that societies tend to place more value on the quality of growth as they become wealthier: with their basic needs met, they can afford to address a broader set of concerns. The Commission’s analysis suggests that countries may want to place greater weight on the quality of growth earlier in their development journey, given the economic costs of air pollution, congestion, land degradation, deforestation, and other problems.

Many of the investments and policies discussed in this report will be particularly valuable to the poorest and most vulnerable people in developing countries: smallholder farmers whose crops are increasingly threatened by land degradation and climate change; the 350 million people who live in (and often depend on) forests; 39 the billions who lack modern cooking facilities, electricity or both; 40 and low-income urban residents who rely on public transport. The low-carbon economy can help reduce poverty and raise living standards in many ways, such as through “climate-smart” agriculture, payments for ecosystem services, off-grid renewable energy solutions, and bus rapid transit (BRT) systems, among many others.

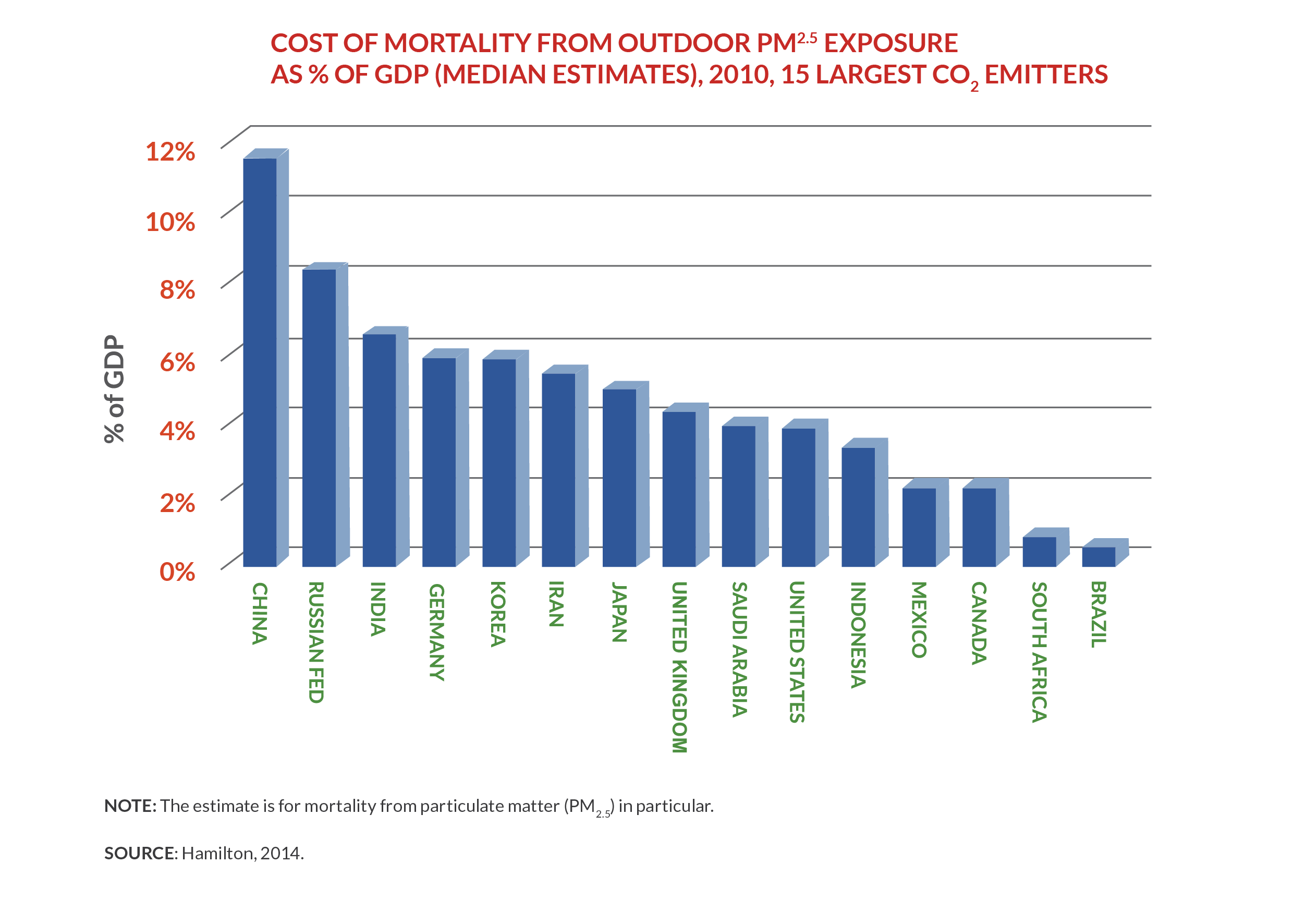

The potential for a low-carbon transition to improve air quality in particular is significant. As noted earlier, rapid economic growth based on fossil fuels has led to severe air pollution in many middle-income countries. New analysis for the Commission values the health and mortality burden of air pollution in the 15 top GHG-emitting countries at an average of 4.4% of GDP (see Figure 3). In China this rises to more than 10% of GDP. 41 Substituting coal by natural gas and especially low-carbon energy sources such as renewables, hydropower and nuclear can therefore lead to major improvements in public health.

Note: The estimate is for mortality from particulate matter (PM2.5) exposure in particular, which was also the focus of recent World Health Organization mortality estimates. Source: Hamilton, 2014. 42

Of course air quality can also be improved by interventions which do not lower GHG emissions, such as “end-of-pipe” pollution controls and relocation of coal-fired power stations and heavy industry away from urban areas. Realising the twin benefits of lower carbon emissions and improved health requires deliberate policy choices. Research carried out for the Commission in China suggests that doing both together is often the most cost-effective option. 43 It is clear that air pollution increases the “real cost” of fossil fuel use. For example, in large parts of Southeast Asia, coal-fired power costs as little as US$60–70 per MWh, but even conservative accounting for air pollution in 2030 adds a cost of US$40/MWh, enough to bridge or exceed the cost gap to alternative power sources. 44

A related example is in urban transport. The Commission’s analysis of urban development planning shows cities that control sprawl and are built around efficient public transport systems can both stimulate economic performance (by reducing traffic congestion, making journeys shorter, and reducing fuel costs) and reduce GHG emissions. 45 But they are also likely to improve air quality, reduce road accidents (a major source of death and injury, particularly in developing countries 46), and generate higher quality of life for residents. This, in turn, can make them more attractive to businesses and their potential employees.

These examples illustrate the potential for a lower-carbon development path to generate multiple benefits. Indeed, for most city authorities and energy and environment ministries now pursuing air quality and urban development policies throughout the world, climate change is rarely the primary reason for taking action. The reduction in carbon emissions is in effect a co-benefit of policies designed to meet other economic and social goals.

Like development more generally, low-carbon growth can increase or reduce vulnerability to climate change, depending on the choices made. 47 A crucial first step is to “climate-proof” low-carbon investments – to ensure that new infrastructure, for example, is resilient to future climate change, and that it does not leave people more vulnerable to hazards. In some cases, simple precautions will suffice, such as avoiding construction in areas prone to flooding or landslides; at other times projects may prove unviable, such as a hydropower station on a river with diminishing flows. There are also potential measures with multiple benefits: increasing resilience, supporting growth and lowering emissions. For example, climate-smart agriculture practices such as minimising tillage and planting trees on and around farmland can boost crop yields, reduce the need for inputs, increase soil carbon storage, and reduce vulnerability to drought. 48 In general, there is a strong convergence between the goals of low-carbon development and environmental sustainability.

The processes of economic change discussed in this report contain four sets of variables that standard economic models do not handle well, either individually or in combination: the processes of structural transformation, the dynamics of technological change and innovation, the local and global economic impact of growing climate risk, and the valuation of non-market outputs (such as better air quality), including the trade-off with market outputs.

There is growing evidence to suggest that such models tend to overestimate the costs of climate action and underestimate the benefits. Yet even recognising this bias, the models suggest that growth and climate action can work together. In the short term, most economic models show that low-carbon pathways have higher initial rates of investment, which reduce current consumption, but have the potential to raise consumption in the medium- to long term. Some economic models that allow for efficient, fiscally neutral recycling of carbon revenues tend to show low-carbon policy (such as carbon pricing) only slightly reducing or actually increasing growth rates, even in the short run. 49

In the longer term, even so-called “general equilibrium” models (which rather unrealistically assume that economies operate at more or less perfect efficiency at all times, and struggle to integrate the dynamic increasing returns associated with disruptive technological change), predict that the difference between global GDP in low- and high-carbon scenarios by around 2030 is only around 1–4%. 50 Given how much the economy will have grown by then, that is not large: it is equivalent to reaching the same level of GDP 6–12 months later. 51 Those models which have attempted to incorporate the impacts of climate change itself show, perhaps unsurprisingly, that global GDP could perform better in lower-carbon scenarios than in higher-carbon ones, as the costs of climate impacts in the latter grow over time. 52

Economic modelling also suggests that low-carbon policies will create employment opportunities in some sectors, while in others, they will be lost (or not created). But most models suggest that the overall effects, even of strong low-carbon policies, are small, generally around plus or minus 1–2% of total employment. They depend partly on the kinds of policies adopted: some analyses suggest that using carbon pricing revenues to cut other, distortionary taxes can lead to net growth in employment in some cases. Other models show small net losses. In both cases the impact of low-carbon policy is dwarfed by the much larger effects of macroeconomic and labour market policies, and changes in the structure of economies. 53

But the fact that in relation to the economy as a whole, the net employment impacts of low-carbon policies are small does not mean that they are unimportant. On the contrary, in some sectors, the impact on jobs is likely to be significant. 54 Employment in the coal sector, which is still relatively labour-intensive in developing countries but already highly mechanised in developed economies, will almost certainly decline even beyond the job reductions that technological change would anyway cause. Employment in heavy and energy-intensive industrial sectors is also likely to be affected, as the shift to a low-carbon economy would probably shrink the relative share of these industries in the economy over the long term. At the same time, the relative value of companies involved in the fossil fuel sector in general (oil and gas as well as coal) is likely to decline over time, as future demand falls.

There is no doubt that this will create real challenges in countries where these sectors are important. Governments may need to support affected industrial sectors in developing new lower-carbon strategies, particularly to exploit the potential for technological innovation in products and processes. 55 Owners of fossil fuel assets (including governments and pension funds), and public authorities dependent on tax revenues and royalties from these sectors, will need to develop long-term transition strategies. These processes will be gradual, taking place over decades, but the earlier they are set in motion, the lower the costs will be.

There will also be many job gains. The evidence shows that investment in low-carbon energy sources and energy efficiency is a major source of job creation. For example, the International Renewable Energy Agency (IRENA) estimates that almost 6 million people were directly employed in the renewable energy sector in 2012, including over 1.7 million in China. 56 This is approaching the number of people employed in the coal industry. 57 As developed countries have adopted low-carbon measures, there has been a little-noticed but remarkable growth in employment in a wide range of businesses in the “low-carbon sector”. 58 As the transition to a lower-carbon economy accelerates, this pattern of job creation and business expansion is likely to be replicated more widely.

These relative shifts in employment between sectors will require active management by governments to ensure the political viability of a low-carbon transition. Explicit measures will be need to be implemented to support and compensate workers displaced as a consequence of the shift towards a lower-carbon economy, and communities affected by industrial decline. 59 These might include direct financial assistance, retraining and reskilling, and investment in community economic development. 60

Strategies of these kinds to achieve a “just transition”, tailored to different sectors in different countries, will need to be developed by governments at both the national and sub-national levels. More generally, it will be important for economic policies to encourage and support the redeployment of both labour and capital into new and growing sectors as others decline. Such policies, including those which stimulate open and competitive markets, are not only good for growth, but will also significantly reduce the costs of adjustment to a low-carbon economy.

“Just transition” strategies will also need to ensure that support is provided to low-income households affected by rising energy and resource prices. Higher prices are the likely consequence of two kinds of policies which the Commission argues will be essential for a low-carbon transition: the phase-out of fossil fuel subsidies, and the introduction of carbon pricing. The Commission fully recognises the political difficulties associated with such policies. It is particularly sensitive to the challenges faced by low-income countries, given their more limited institutional and financial resources, and the urgency of addressing extreme poverty.

However, the Commission is also encouraged by success stories in both developed and developing countries. Ghana and Indonesia, for example, have succeeded in reducing fossil fuel subsidies by using part of the revenues released to provide conditional cash transfers and other forms of financial assistance to low-income households. 61 A number of countries and states, such as Sweden and British Columbia in Canada, have used the revenues from carbon pricing policies or other sources of expenditure to compensate households and to subsidise energy efficiency measures, which can help cut overall energy bills. 62

Social protection policies of these kinds designed to manage the transition to a lower-carbon economy in a fair way are integral components of the policy toolkit which governments will need. Experience in almost all countries which have been through a process of economic restructuring shows that it is the distributional impacts on those sectors and communities adversely affected by change which make them politically tough to carry through. Every country will need to find its own context-specific strategies to manage these consequences.

The transition to a lower-carbon economy will be particularly difficult for low-income countries whose principal challenge remains the reduction of poverty. The Commission strongly believes that the developed world has an obligation to provide developing countries with additional financial, technical and capacity-building support to enable them to finance lower-carbon and more climate-resilient investment strategies.

Developing countries will especially need support in financing capital-intensive low-carbon and climate-resilient infrastructure assets. This reinforces the need for good, predictable regulatory arrangements which can attract private capital, alongside flows of long-term, concessional, international public climate finance. International climate finance flows need to increase sharply if climate risk is to be reduced and developing countries are to achieve lower-carbon and more climate-resilient development paths. The developed countries will need to set out a pathway to show how they will achieve their agreed goal of mobilising US$100 billion per year in public- and private-sector finance by 2020.

The analysis conducted for the Commission suggests that, in many of the most crucial fields of growth over the coming 10–15 years, there are significant actions and policies which can drive both strong economic performance and reductions in the trajectory of GHG emissions. But how far can emissions be reduced by these methods? Would this be enough to prevent what the international community has described as the risk of “dangerous” climate change? 63

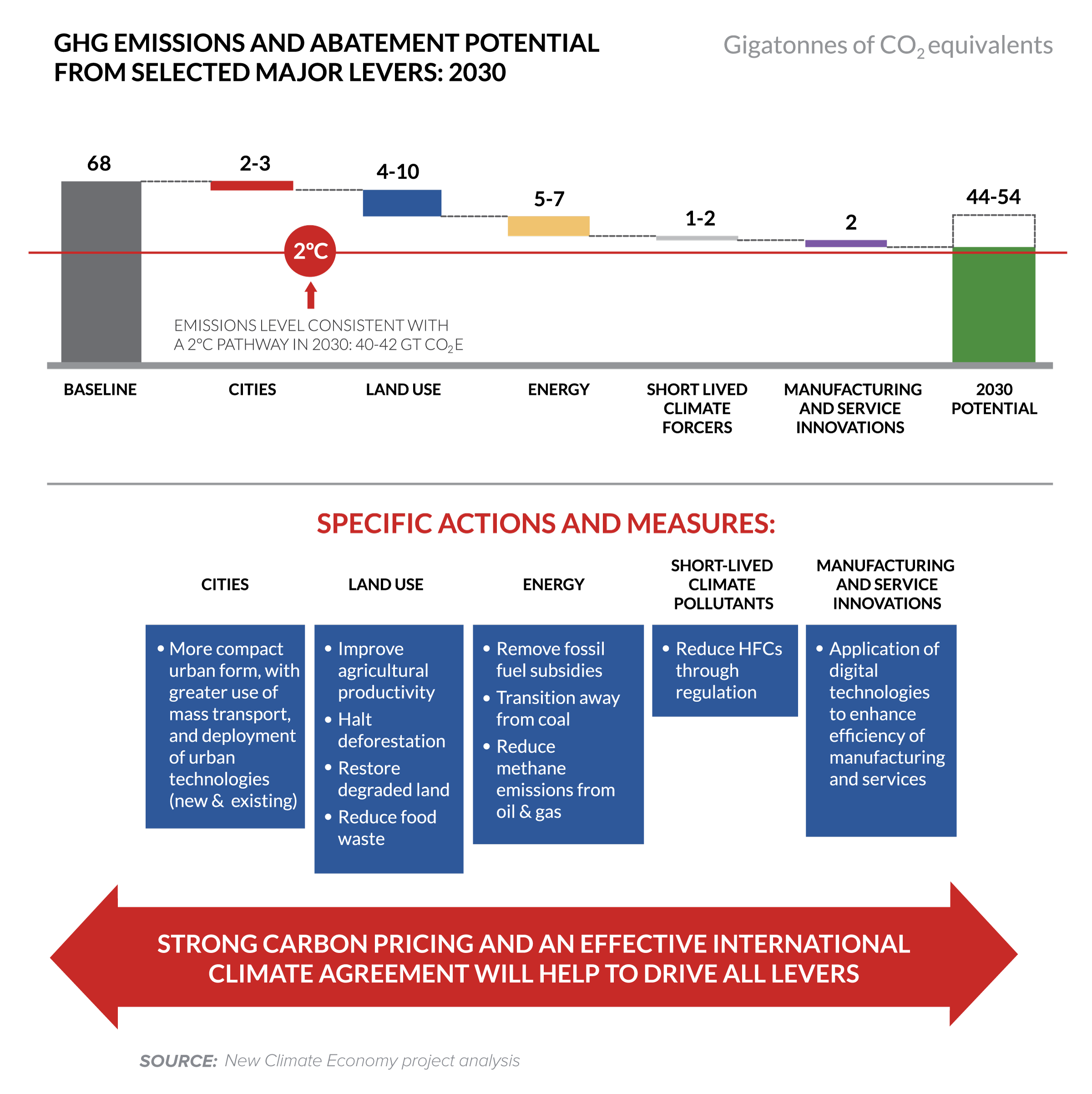

Answering this question requires, first, an idea of the trajectory of emissions which would be consistent with the international goal of holding the average global temperature rise to no more than 2°C above pre-industrial times. The Intergovernmental Panel on Climate Change (IPCC)’s review of recent emission projections suggests that if current trends continue, global emissions in 2030 will be around 68 Gt CO2e, compared with around 50 Gt CO2e today. 64 To have a likely (more than two-thirds) chance of holding the average global temperature rise to 2°C, the IPCC suggests that by 2030, global emissions should be no more than 42 Gt CO2e per year. That would require a reduction in emissions over the “base case” of 26 Gt CO2e by 2030.

To achieve this target, the carbon productivity of the world economy (defined in terms of US$ of world output/tonnes of GHG emissions) would need to increase by about 3–4% per year until 2030, compared with a historic 25-year trend of around 1% per year. 65 In 2030–2050, the improvement in carbon productivity would need to accelerate again, to around 6–7% per year, to stay on track. 66

Against this background, the Commission’s research programme has sought to calculate the emissions reductions which the most significant measures and actions set out in this report might have the potential to achieve by 2030, compared with the standard “base case”. All of the actions included in these calculations – in the fields of urban development, land use change, energy investment and specific forms of innovation in manufacturing and services – have multiple economic benefits. That is, all of them provide benefits not just in terms of standard economic indicators, but in other welfare-enhancing factors, such as reductions in rural poverty, improvements in health from better air quality, lower urban traffic congestion and the protection of ecosystem services. While some may have a small net cost considered in narrow economic terms, all can therefore make a strong claim to contribute to higher-quality growth. Another way of putting this is that governments, cities and businesses would have strong reasons to implement them even without consideration of their climate change benefits.

In total, the emissions reductions estimated to be available from the principal measures and actions described in this report add up to 14–24 Gt CO2e, depending on the extent to which the measures are implemented (see Figure 4). This range is equivalent to at least 50% and potentially up to 90% of the emissions reductions needed by 2030, as discussed above, for a two-thirds or better chance of keeping global average warming below 2°C. It must be stressed that the high end of the range would require early, broad and ambitious implementation of those measures and actions. That, in turn, would require decisive policy change and leadership, and rapid learning and sharing of best practice, combined with strong international cooperation, particularly to support developing countries’ efforts.

Calculations of this kind cannot be precise, which is why the figures come with a broad range. They depend on assumptions about what happens in the “base case”, how far specific kinds of measures can be implemented and at what cost, the level of emissions they will generate, the underlying economic conditions (including growth rates and energy prices), and how rapidly technological changes may occur. They also depend on judgements of how the multiple economic benefits of these measures and actions should be valued. But with all these caveats, the figures do provide an indication of the scale of reductions potentially available.

On their own, these measures would not be sufficient to achieve the full range of emissions reductions likely to be needed by 2030 to prevent dangerous climate change. But this report has not sought to examine every currently available option for emissions reduction. By the second half of the 2020s, technological change will almost certainly have led to new possibilities not known today. Thus, it is more or less impossible to estimate the economic costs and benefits of all the additional emissions reductions which may be required by 2030.

But it is clear that achieving the total mitigation needed may require actions with net economic costs. Buildings will have to be more deeply retrofitted with energy efficiency measures than could be justified otherwise. Coal- and gas-fired power stations will have to be retired early, or fitted with carbon capture and storage (CCS) technology whose sole purpose is the reduction of greenhouse gas emissions. Industrial, agricultural and transport emissions will need stronger reductions. These costs will be the “pure” costs of reducing severe climate risk, justifiable only for that reason.

Most of the economic models which have attempted to estimate the net costs of achieving a likely 2°C pathway suggest that they are relatively small, amounting to 1–4% of GDP by 2030. 68 They are almost certainly outweighed by the future economic damages associated with warming of more than 2°C that they would avoid. Still, the likelihood that actions with net costs will be needed suggests that investment in R&D on key technologies such as CCS should be scaled up considerably today.

The areas on which this report focuses involve the fundamental drivers of both growth and emissions over the long term. The low-carbon transition will not end in 2030. Much deeper reductions will be required in later years, to take global emissions down to less than 20 Gt CO2e by 2050 and near zero or below in the second half of the century.69 The measures and actions proposed in this report would help countries lay the groundwork by 2030 – in urban policy and design, land use, energy systems, economic policy, finance and technological innovation – to facilitate further climate action from 2030 onward.

The research undertaken for the Commission has sought to arrive at some broad, preliminary estimates of the scope for countries to undertake reforms and investments that are likely to yield significant economic, health and other benefits, while also helping curb greenhouse gas emissions. It draws upon a survey of relevant technical literature to arrive at monetary estimates of the multiple benefits per tonne of CO2 abated, related to the following actions:

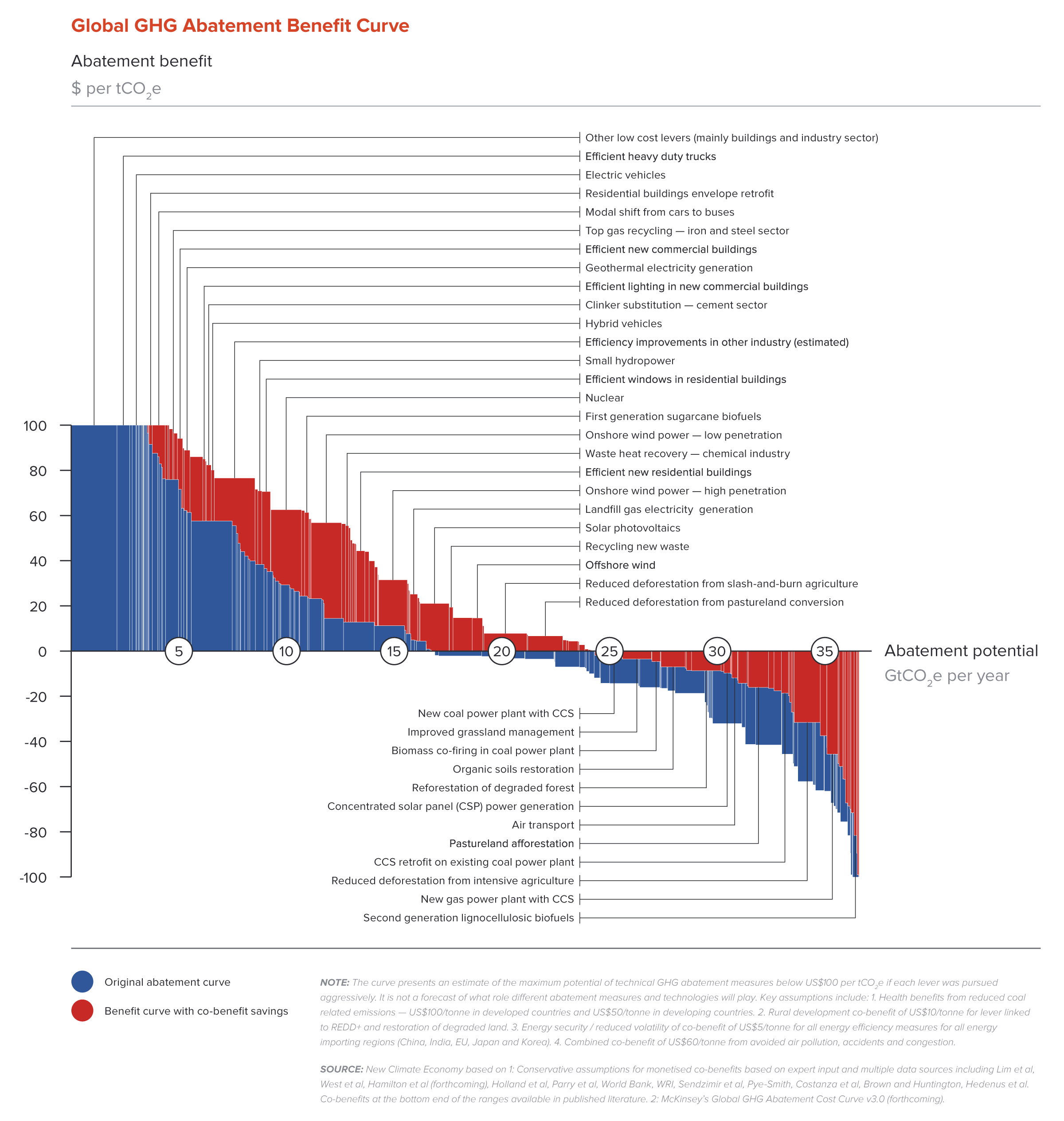

The results are presented by adjusting the Marginal Abatement Cost Curve (MACC) developed by McKinsey & Company. 71 Each of the blue bars in Figure 5 shows the estimated incremental cost in 2030, relative to the high-carbon alternative, of abating an extra tonne of CO2 through a specific technique or action, and the total technical abatement potential it offers. The incremental cost estimate per tonne in 2030 is based on the difference in operating and annualised capital costs between the low- and high-carbon alternatives, net of any potential savings associated with the shift to low-carbon. The red bars show the additional co-benefits associated with various abatement options, such as the health benefits from reduced local air pollution. The original McKinsey cost curve is inverted, so that methods with net benefits appear above the axis and those with net costs below, and the value of the multiple benefits is included where relevant. Thus, the chart becomes a “marginal abatement benefits curve”.

The curve shows that not only are there many abatement options that create net benefits in narrow economic terms, but there are many more – and the economic welfare gain becomes significantly larger – once co-benefits are included. A number of options with net costs in the “narrow” sense become net benefits when co-benefits are taken into account, such as reduced deforestation, recycling of new waste, and offshore wind. For energy-efficiency options, the inclusion of co-benefits can as much as triple the overall benefit.

The quantification of co-benefits undertaken here is of an exploratory nature. The coverage of co-benefits is incomplete, and various implementation issues have not been taken into account. The approach does not incorporate transaction costs, nor does it attempt to show how different sequencing or combinations of measures might give better overall results. However, it does provide a directional sense of which measures might be more attractive and cost-effective, as well as their rough contribution to meeting 2030 abatement goals. The analysis strengthens the case that policy-makers have a broad array of reform and investment options to further economic welfare while abating GHG emissions. This analysis may be particularly helpful for highlighting options where narrowly defined economic benefits are low or negative, but where the co-benefits are significant.

The case for acting to drive growth and climate risk reduction together is very strong. But time is not on the world’s side. The next 10-15 years will be critical.

Major shifts in the structure of economies are not unprecedented. Over the last 30 years, many developed and developing countries have undergone structural economic transformations. The evidence suggests that both well-functioning markets and well-governed public institutions are vital. Public debate, broad political support and thriving civil society organisations can make a huge difference to the chances of success.

The role of businesses in this transition is particularly important. Many companies, of all sizes in all countries, have already begun to move onto low-carbon and climate-resilient paths. Many of those that have gone furthest have found the outcomes powerfully positive for their “bottom lines”, reducing input costs, stimulating innovation and helping to address other risks. 73 Many business actions require government regulation or incentives to make them feasible – but it is incumbent on responsible companies to support the adoption of those policy frameworks, rather than oppose them, as is often the case. Many companies have made progress in reporting on their environmental and social impacts. But such reporting remains optional and in many cases partial. It now needs to be standardised and integrated into core financial reporting requirements.

This needs to be part of a more comprehensive reframing of the rules and norms of economic life. The metrics which governments, businesses, finance institutions and international organisations use to assess their performance, and the risks to which they are exposed, need routinely to incorporate a more sophisticated understanding of how economic and business outcomes relate to environmental impact. 74

Above all, a global transition to a low-carbon and climate-resilient development path will need to be underpinned by an international agreement committing countries to this collective economic future. Such an agreement could act as a powerful macroeconomic instrument, reinforcing domestic policy and sending a strong and predictable signal to businesses and investors about the future direction of the global economy. The signalling effect of such an agreement would be valuably increased if it included a long-term goal to reduce net GHG emissions to near zero or below by the second half of this century. 75 The agreement must be equitable, and developed countries must provide strong climate finance to developing countries, for adaptation, mitigation and capacity-building.

Each chapter of this report makes recommendations in specific areas of policy and action; several are included in the summaries in Part II. The recommendations have been distilled into a 10-point Global Action Plan, presented in Part III.

The wealth of evidence presented by this report shows that there is now huge scope to meet countries’ economic and social goals while also reducing climate risk. Economic leaders have a remarkable opportunity to achieve better growth and a better climate.

Cities are crucial to both economic growth and climate action. Urban areas are home to half the world’s population, but generate around 80% of global economic output, 76 and around 70% of global energy use and energy-related GHG emissions. 77 Over the next two decades, nearly all of the world’s net population growth is expected to occur in urban areas, with about 1.4 million people – close to the population of Stockholm – added each week. 78 By 2050, the urban population will increase by at least 2.5 billion, reaching two-thirds of the global population. 79

The stakes for growth, quality of life and carbon emissions could not be higher. The structures we build now, including roads and buildings, could last for a century or more, setting the trajectory for greenhouse gas emissions at a critical time for reining these in.

Given the long-lived nature of urban infrastructure, the way in which we build, rebuild, maintain and enhance the world’s growing cities will not only determine their economic performance and their citizens’ quality of life; it may also define the trajectory of global GHG emissions for much of the rest of the century. This chapter takes stock of cities’ increasing contribution to both economic growth and climate change, examines the dominant patterns of development today, and presents an alternative pathway, as well as the policies needed to support and scale it up.

We focus in particular on three categories of cities:

Research carried out for the Commission shows that, on current trends, these cities combined will account for 60% of global GDP growth between now and 2030. They will account for close to half of global energy-related GHG emissions. Some 300 emerging cities, with populations between 1 million and 10 million, will account for over half of this growth. The question for mayors, as well as for policy-makers in economics, finance, urban planning and environmental ministries, is how to plan urban development in a way that improves economic performance and quality of life while reducing GHG emissions.

A large share of urban growth around the world involves unplanned, unstructured urban expansion, with low densities and high rates of car use. If current development trends were to continue, the global area of urbanised land could triple from 2000 to 2030, 80 the equivalent to adding an area greater than the size of Manhattan every day. At the same time, the number of cars could double, from 1 billion today to 2 billion. 81

This sprawling pattern of expansion has major costs. It can double land used per housing unit, increase the costs of providing utilities and public services by 10–30% or more, and increase motor travel and associated costs by 20–50%. 82 In fast-growing low- and middle-income countries, sprawled patterns can actually double or triple many costs, because they often have to import construction equipment. Sprawl also results in greater congestion, accident and air pollution costs; locks in inefficiently high levels of energy consumption, and makes it harder to implement more efficient models of waste management and district heating.

New modelling for this report shows that the incremental external costs of sprawl in the United States are about US$400 billion per year, due to increased costs of providing public services, higher capital requirements for infrastructure, lower overall resource productivity, and accident and pollution damages. 83 Costs can be even more acute in rapidly urbanising countries where resources are more limited. In China, urban sprawl has reduced productivity gains from agglomeration and specialisation, and led to much higher levels of capital spending than necessary to sustain growth. 84 Research from 261 Chinese cities in 2004, for example, suggested that labour productivity would rise by 8.8% if employment density doubled. 85

New analysis reviewed by the Commission shows that even in this context, cities around the world have significant opportunities in the next 5–10 years to boost resource productivity and reduce GHG emissions through economically attractive investments in the buildings, transport and waste sectors. However, without broader structural shifts in urban design and transport systems, the benefits of those measures would quickly be overwhelmed by the impacts of sustained economic and population expansion under business-as-usual patterns. In fast-growing Emerging Cities in particular, the evidence suggests energy savings and emission reductions could be erased within five years or less. 86

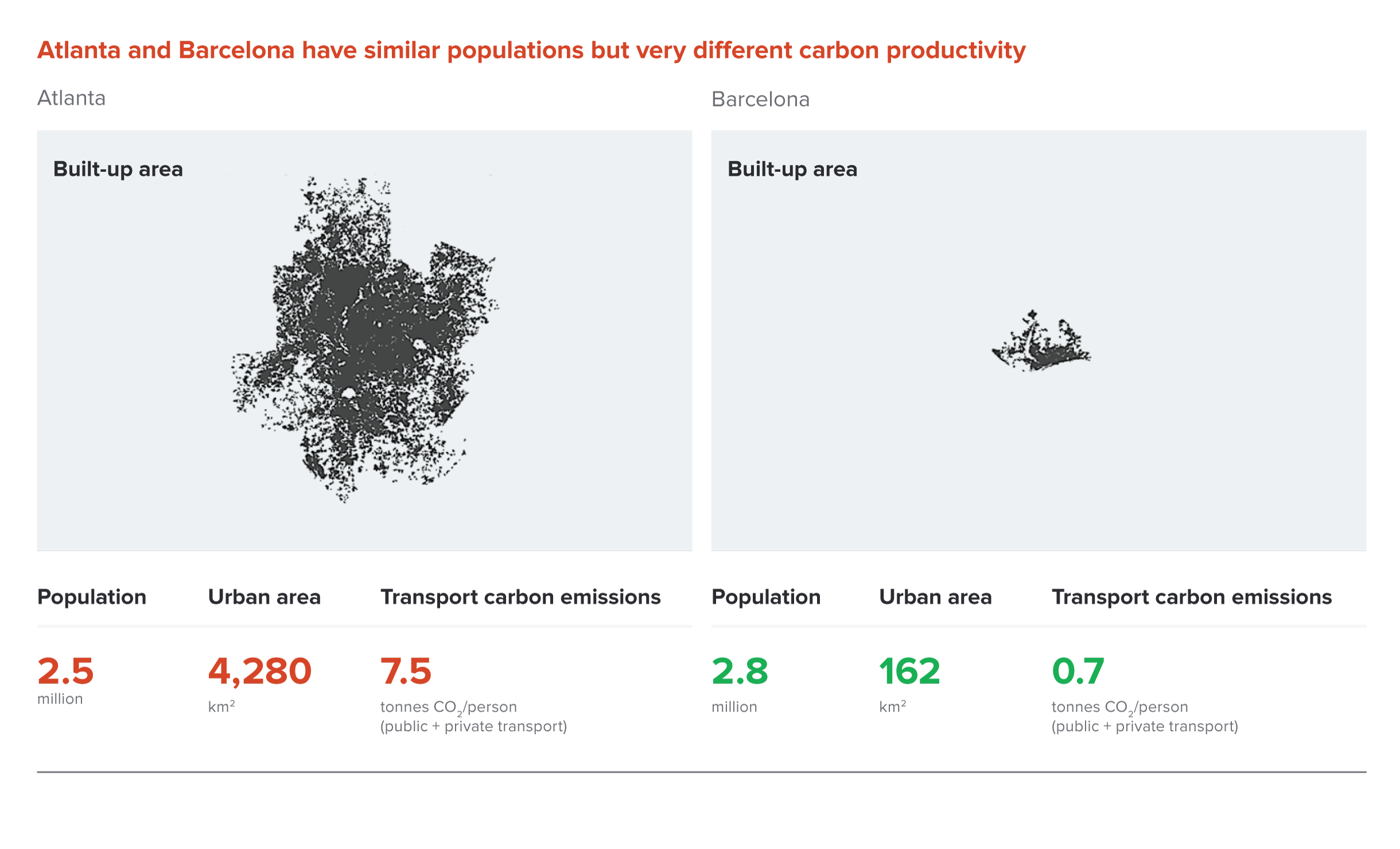

Thus, to unlock a new wave of sustained, long-term urban productivity improvements, we need a systemic shift to more compact, connected and coordinated development. Cities that meet these criteria are more productive, socially inclusive, resilient, cleaner, quieter and safer. They also have lower GHG emissions – a good example of the benefits of pursuing economic growth and climate change mitigation together. Figure 6, for example, contrasts the land use and GHG implications of urban development patterns followed in the US city of Atlanta and in Barcelona, Spain.

Bertaud, A. and Richardson, A.W (2004), Transit and density: Atlanta, the United States and Western Europe, Figure 17.2 on p.6, available at http://courses.washington.edu/

Kenworthy (2003), Transport Energy Use and Greenhouse Gases in Urban Passenger Transport Systems: A Study of 84 Global Cities, Third Conference of the Regional Government Network for Sustainable Development, Notre Dame University, Fremantle, Western Australia, September 17-19, 2003. Figure 1 on p.18 cited in Lefevre, B. (2009), Urban Transport Energy Consumption: Determinants and Strategies for its Reduction, S.A.P.I.EN.S 2(3): 1–32. Figure 6, available at http://sapiens.revues.org/914]

The alternative to unplanned, unstructured urban expansion is a more efficient urban development model, based on managed growth which encourages higher densities, mixed-use neighbourhoods, walkable local environments, and – in Global Megacities and Mature Cities – the revitalisation and redevelopment of urban centres and brownfield sites, complemented by green spaces. This model prioritises high-quality public transport systems to make the most of compact urban forms and to reduce car dependence and congestion. It also boosts resource efficiency through “smarter” utilities and buildings. It has the potential to reduce urban infrastructure capital requirements by more than US$3 trillion over the next 15 years. 87 Fast-growing Emerging Cities and small urban areas have a particularly important opportunity to adopt this model from the outset, learning from others’ experience.

Shifting towards this alternative model would unlock significant medium- to long-term economic and social benefits. It would boost infrastructure productivity through the agglomeration effects of greater density, improve air quality, and deliver substantial cost savings in the transport sector. Estimates for the United States suggest that transit-oriented urban development could reduce per capita car use by 50%, reducing household expenditures by 20%. 88 At significantly lower fuel prices, sprawling Houston spends about 14% of its GDP on transport compared with 4% in Copenhagen and about 7% in many Western European cities. (Notably, Houston is now making ambitious efforts to overcome the legacy of sprawl through urban renewal and sustained investment in public transport systems.) 89

Adopting a compact, transit-oriented model in the world’s largest 724 cities, new analysis for the Commission shows, could reduce GHG emissions by up to 1.5 billion tonnes CO2e per year by 2030, mostly by reducing personal vehicle use in favour of more efficient transport modes. While achieving such savings would require transformative change, it would lay the foundation for even greater, sustained resource savings and emission reductions over the following decades.

In fact, such a shift is already happening. Re-densification is taking place in cities as diverse as London, Brussels, Tokyo, Hamburg, Nagoya and Beijing. More than 160 cities have implemented bus rapid transit (BRT) systems, which can carry large numbers of passengers per day at less than 15% of the cost of a metro.90 The BRT in Bogotá, Colombia, for example, carries up to 2.1 million passengers per day, complemented by a citywide network of bicycle paths that connect residents to public transport, community spaces and parks. 91 China will have 3,000km of urban rail networks by 2015.92 Nearly 700 cities had bike-sharing schemes at the end of 2013, up from five in 2000.93

From Copenhagen, to Hong Kong, to Portland, Oregon, in the US, cities are also showing how they can build prosperity, improve air quality, reduce GHG emissions all at once through more compact, connected and coordinated urban growth models. Stockholm reduced emissions by 35% from 1993 to 2010 while growing its economy by 41%, one of the highest growth rates in Europe. 94 Curitiba is one of the most affluent cities in Brazil, but has 25% lower per capita GHG emissions and 30% lower fuel consumption than the national average due to its groundbreaking approach to integrated land use and transport planning. 95

Countries need to prioritise better-managed urban development and increased urban productivity as key drivers of growth and climate goals. This is especially the case for countries with rapidly urbanising populations, as current institutional arrangements often result in urban development being driven by other national priorities. Here, coordination and cooperation between national and regional governments and city leaders is essential.

Several countries are already making major policy changes to promote more compact, mixed-use land development, contain urban sprawl, maximise resource efficiency, and curtail the negative externalities of pollution, congestion and CO2 emissions. A high-profile example is China’s New National Urbanisation Plan, which places urban policy at the heart of Chinese decision-making. 96

They should also provide greater fiscal autonomy for cities, potentially linked to economic, social and environmental performance benchmarks, and consider setting up a special-purpose financing vehicle at the national level to support cities’ efforts to become more compact, connected and coordinated, with appropriate private-sector participation. Existing infrastructure funding should be redirected to support this transition.

Building better, more productive cities is a long-term journey. It requires persistence in several key areas to shift away from business-as-usual urban expansion, with countries, regions and cities working together. As a first step, cities should seize some of the numerous opportunities available to boost resource productivity in the short- to medium term, in sectors as diverse as buildings, transport and waste management. The evidence suggests that these smaller steps could build momentum for broader, longer-term reform, especially in capacity-constrained cities.

Only about 20% of the world’s 150 largest cities have even the basic analytics needed for low-carbon planning. 97 These efforts should be supported by regulatory reform to promote higher-density, mixed-use, infill development, and new measures such as efficient parking practices.

It is also crucial to change transport incentives.

They should also consider charges on land conversion and dispersed development, and measures that place a higher price on land than on buildings such as land taxes and development taxes. These reforms can raise revenue to invest in public transport and transit-oriented development.

In addition, there is a need for new mechanisms to finance upfront investments in smarter urban infrastructure and technology, such as greater use of land value capture, municipal bond financing, and investment platforms to prepare and package investments to attract private- sector capital. This should be complemented by more effective and accountable city-level institutions. The chapter discusses these topics in detail.

The international community also has a key role to play in fostering better-managed urban growth, both by building and sharing knowledge about best practices, and by steering finance towards compact, connected and coordinated urbanisation, and away from sprawl.

The initiative should: build on the existing work of key international organisations already working in this field, including city networks such as C40 and ICLEI (Local Governments for Sustainability), and involve rapidly urbanising countries, mayors and business leaders. Key activities could include reviewing institutional options for systematic collection of city-level data, developing urbanisation scenarios and best practice guidance, creating an international standard for integrated municipal accounting, and targeted capacity-building.

Only 4% of the 500 largest cities in developing countries are now deemed creditworthy in international financial markets; every US$1 spent to correct this can leverage more than US$100 in private-sector finance. 98 The new facility should build on and scale-up the existing programme of the World Bank, and assist cities in both developing and developed countries.

The banks should work with client and donor countries to redirect overseas development assistance and concessional finance towards supporting integrated citywide urban strategies and investment in smarter infrastructure and new technology. Greater consideration should also be given to redirecting overall MDB funding to account for the growing importance of cities in economic development in rapidly urbanising countries, as well as the scaling-up of support to help cities prepare and package urban infrastructure investments.

Rapid global population growth, urbanisation, rising incomes and resource constraints are putting enormous pressure on land and water resources used by agriculture and forests, which are crucial to food security and livelihoods. Roughly a quarter of the world’s agricultural land is severely degraded, 99 and forests continue to be cleared for timber and charcoal, and to use the land for crops and pasture. 100 Key ecosystem services are being compromised, and the natural resource base is becoming less productive. At the same time, climate change is posing enormous challenges, increasing both flood and drought risk in many places, and altering hydrological systems and seasonal weather patterns.

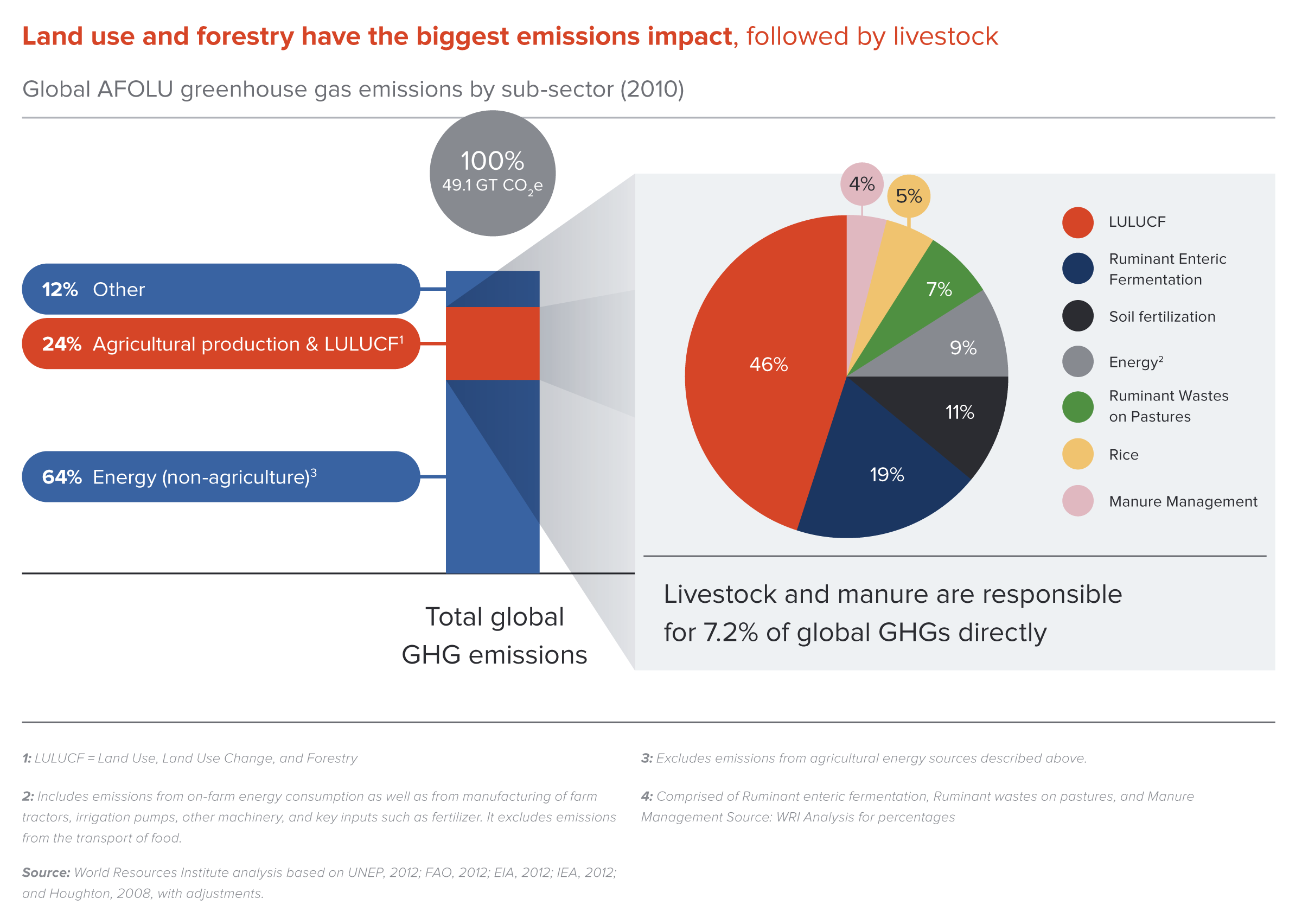

Agriculture, forestry and other land use also account for a quarter of global GHG emissions. 101 Deforestation and forest degradation alone are responsible for about 11% of global GHGs, net of reforestation; 102 the world’s total forest land decreased by an average of 5.2 million ha per year over 2000-2010. 103 Emissions from agriculture, in turn, include methane from livestock, nitrous oxide from fertiliser use, and carbon dioxide (CO2) from tractors and fertiliser production (see Figure 7).

Source: World Resources Institute analysis based on UNEP, 2012; FAO, 2012; EIA, 2012; IEA, 2012; and Houghton, 2008, with adjustments. 104

Those factors combined make agriculture and forests top-priority sectors for climate policy, particularly in tropical countries, which often include substantial areas of carbon-rich forest. They are also crucial to many developing economies: in countries in the US$400–1,800 per capita GDP range (2005$), many of them in Asia, the World Bank found agriculture was 20% of GDP on average; in sub-Saharan Africa, it was 34%, and accounted for almost two-thirds of employment and a third of GDP growth in 1993–2005.105 Globally, 70% of the poorest people live in rural areas and depend on agriculture for their livelihoods, mostly in the tropics. 106

Developing countries are also where more than 80% of the global demand growth for agricultural and forest products will occur over the next 15 years. 107 By 2050, the world’s farms will need to produce 70% more calories than in 2006, mainly due to population growth, rising incomes and changing diets in developing countries. 108 Meeting this new demand will be critical to growth, food security and poverty alleviation; it will also create huge opportunities for businesses – from small farms and local businesses, to multinationals. How this demand is met will be critical to climate outcomes.

The “Green Revolution”– a multi-decade effort to modernise farming in the developing world – boosted crop yields, by developing high-yield grain varieties and sharply increasing the use of agricultural inputs (irrigation water, fertilisers). Many of the measures needed today are more location-specific, addressing issues such as drought, floods, pests and saltwater intrusions. There are already promising innovations, such as “Scuba rice”, which can withstand submersion in water, a common situation as floods increase in South and Southeast Asia. The variety was introduced in India in 2008 and has since been adopted by 5 million farmers in the region.109

For major cereal crops, the research supported by the Consultative Group on International Agricultural Research (CGIAR), a US$1 billion-a-year global partnership, will be invaluable. Public-sector support in individual countries is also crucial, particularly for rice and “orphan crops”– some starchy root crops, vegetables, legumes, etc. – that have little global market value but are local dietary staples. Yet in 2008, governments only spent US$32 billion on agricultural R&D – including US$15.6 billion (2005 PPP) in developing and emerging economies. Private-sector funding added another US$18 billion (2005 PPP), primarily in developed countries.110

There is considerable scope to increase funding for agricultural R&D to increase productivity and resilience, whether through multilateral, regional or national institutions.

One way to free up funds for R&D is to reduce input subsidies (mainly for fertiliser and water). Agricultural subsidies in China rose to US$73 billion in 2012, or 9% of agricultural output; 111 India provided roughly US$28 billion in input subsidies to nitrogenous fertilisers and electricity for pumping agricultural water in 2010. 112 OECD country governments paid farmers US$32 billion based on input use in 2012. 113 Many countries subsidise inputs to try to boost productivity, but they can also lead to waste and environmental damage.

This would incentivise better, more targeted input use, reduce associated pollution and GHG emissions, and save farmers money, since they pay for inputs even if they are subsidised. Potential GHG emission reductions of 200 million tonnes of CO2e per year have been estimated from more efficient use of fertilisers in China alone, 114 and close to 100 million tonnes of CO2e per year from more efficient use of water in India. 115

Halting and reversing land degradation should also be a priority. About one-quarter of agricultural land globally is now severely degraded. 116 Case studies in China, Ethiopia, Mexico, Uganda, Rwanda, Chile and Indonesia found land degradation decreased productivity by 3–7% per year. 117 Well-tested practices can add organic matter to the soil and control water runoff, jointly improving water retention and soil fertility, and increasing carbon storage in soils, plants and trees.

Such approaches consider ecosystems, resource use and human activities across the broader landscape, not just farm-by-farm. They also typically involve planting trees on farms and/or restoring and protecting forested areas around farms. They can be large-scale and capital-intensive, or more narrowly targeted, introducing a handful of proven techniques.

The 1994–2005 Loess Plateau projects in China, which mobilised US$491 million in funding and curbed soil erosion on nearly 1 million ha, are a shining example of large-scale efforts (see figure 8). The projects focused on halting the activities that led to degradation – in particular planting on steep slopes, tree-cutting, and free-range grazing of goats; introduced heavy equipment to build wider and sturdier terraces for grain cultivation, and encouraged farmers to plant trees and to allow marginal land to grow wild again. The projects sharply increased grain yields and lifted more than 2.5 million people out of poverty. Soil carbon storage also increased, mostly due to the restoration of forests and grassland. 118 The project model has since been scaled up to cover large areas of the country, through China’s US$40 billion “Grain for Green” programme.119

Source: World Bank project completion evaluations of the Loess Plateau Watershed Habilitation Projects I and II, 1999 and 2005. 120

The Maradi and Zinder regions of Niger, meanwhile, show what can be achieved even at a low cost. Farmers interplanted nitrogen-fixing trees on cropland, or allowed roots and stumps to regenerate, increasing tree and shrub cover 10- to 20-fold. Agricultural productivity was significantly increased on 5 million ha of severely degraded farmland, 121 and biodiversity and soil fertility improved across the entire area. Real farm incomes more than doubled, stimulating local non-farm services as well. 122 Similar conditions exist on another 300 million ha of drylands in Africa alone, suggesting considerable potential for scaling.123

Perceptions of increasing climate and market risk following the food price spikes of 2008 have made both governments and smallholder farmers overly risk-averse in the poorer countries. This has hindered adoption of market-oriented policies, investments and technologies that may be essential for sustained increases in farm income. However, failure to pay attention to increased uncertainty can also be catastrophic for the poor. Solid institutions and leadership are needed to encourage collective action; appropriate incentives and more secure property rights are also crucial.

Forests also need much better protection. Demand for timber, pulp and bioenergy is projected to grow over the next 15 years, putting even more pressure on lands currently supporting natural forests. 124 Projections to 2050 indicate a threefold increase in wood removals by volume compared with 2010. 125 Increasing the profitability of alternative land uses, such as through agricultural intensification, also increases pressures to clear land. Yet the value generated by agriculture in former forestlands and by the extraction of forest products also brings costs. Forests are an important form of natural capital, generating economic returns (and climate benefits) for countries, companies and citizens. The ecosystem services that forests provide are especially important to the resilience of agricultural landscapes. Thus, protecting remaining natural forests and restoring forest cover –globally and in individual regions –is a key part of feeding the world and building a resilient economy.

Millions of hectares of forest are being lost or degraded each year, due to agricultural expansion, timber harvesting, extraction for fuelwood or charcoal, mining and road-building. 126 Once trees have been removed, leading to forest degradation, the land is often converted to other uses, such as agriculture –which is what is technically known as deforestation. While forest degradation and deforestation in the forests often go together, the drivers are different and may require differing approaches. 127 The increasing demand for forest products from growth in emerging economies is central to forest degradation, while the decision on whether to allow degraded forest land to regenerate into forest or to convert it to other uses is driven by the financial viability of alternative uses, property rights, and governance of markets and resources.

Problems arise because market prices, tax policies, lending conditions, and commodity procurement practices often do not reflect (or “internalise”) the wider economic value of a forest. These shortcomings are compounded by lack of information, lack of accountability, and in some places, corruption and powerful vested interests. Any form of capital needed to underpin strong economic growth – whether natural, financial or human – cannot be enhanced and used effectively under such market and governance failures.

Policy interventions are needed to address these problems, and there are many successful examples, from Brazil, to Costa Rica, to Korea. Payments for ecosystem services, such as under REDD+, can also play a key role in helping countries preserve their natural capital.

Options for the latter include a results-based REDD+ window (sub-fund) in the Green Climate Fund, 128 or countries counting emission reductions from REDD+ as part of their “nationally determined contributions” under the 2015 climate agreement. Over time, carbon markets are expected to play an increasing role. Law enforcement and the verification necessary for results-based finance are greatly facilitated by the convergence of low-cost satellite imagery, cloud computing, high-speed internet connectivity, smartphones and social media. These are ushering in a new world of “radical transparency”, where what is happening in a far-away forest can now be known close to home.

Ambitious forest restoration targets are needed as well.

This is consistent with Aichi Target 15, which calls for restoring 15% of degraded ecosystems, 129 and could generate net benefits on the general order of US$170 billion per year from watershed protection, improved crop yields, and forest products. 130 Pathways for restoration at this high level would need to include agroforestry and mosaic restoration in agricultural areas (perhaps on degraded steep slopes of limited commercial value), in addition to assisted or natural regeneration of forests. This would sequester about 1–3 Gt CO2e per year, depending on the pathways used and biomes prevalent in the areas restored. 131

To ease pressure on the land, demand-side measures are also important. On a caloric basis, a quarter of the world’s food is now lost or wasted between farm and fork. For example, food waste reduction measures in developed countries could save US$200 billion per year by 2030, and reduce emissions by at least 0.3 Gt of CO2e. 132 Policy-makers should also work to reduce demand for food crops for biofuels and promote a shift in diets, away from red meat especially.

Our report estimates that following the above recommendations in agriculture, forests and land use change would very conservatively yield an abatement range of between 4.2 to 10.4 Gt CO2e per year in 2030, with an expectation of 7.3 Gt CO2e. The main sub-components of this estimate are: boosting agricultural productivity through a focus on “climate-smart agriculture” innovation (0.6–1.1 Gt); improved forest governance and conservation measures to achieve zero net deforestation, supported by REDD+ (1.6–4.4 Gt); restoring 150 million ha of degraded agricultural land and 350 million ha of degraded forest landscapes, for a total of 500 million ha (1.8–4.5 Gt); and reduced food waste (0.2–0.4 Gt).

We are in a period of unprecedented expansion of energy demand. Global energy use has grown by more than 50% since 1990, 133 and must keep growing to support continued development. As much as a quarter of today’s energy demand was created in just the last decade, and since 2000, all the net growth has occurred in non-OECD countries, more than half of it in China alone. 134 Past projections often failed to anticipate these dramatic shifts, which nonetheless have affected the energy prospects of nearly all countries. The future is now even more uncertain, as projections show anything from a 20% to 35% expansion of global energy demand over the next 15 years. 135

A major wave of investment will be required to meet this demand: around US$45 trillion will be required in 2015–2030 for key categories of energy infrastructure. 136 How that money is spent is critically important: it can help build robust, flexible energy systems that will serve countries well for decades to come, or it can lock in an energy infrastructure that exposes countries to future market volatility, air pollution, and other environmental and social stresses. Given that energy production and use already accounts for two-thirds of global GHG emissions, 137 and those emissions continue to rise, a great deal is at stake for the climate as well.

The next 15 years offer an opportunity to create better energy systems that also reduce future climate risk. Achieving this will require a multi-faceted approach. The starting point must be to get energy pricing right, implementing energy prices that enable cost recovery for investment and less wasteful use of energy, and removing subsidies for fossil fuel consumption, production and investment. Other, complementary initiatives also will be required. One key task is to increase resource efficiency and productivity – to make the most of our energy supplies. Some countries have already made significant gains in this regard, but there is much untapped potential. It also will be necessary to expand our energy supply options. Innovation in technology, as well as business models, financing systems, and regulatory frameworks, is already doing this, from unconventional gas and oil, to the rapid growth of renewable energy technologies.

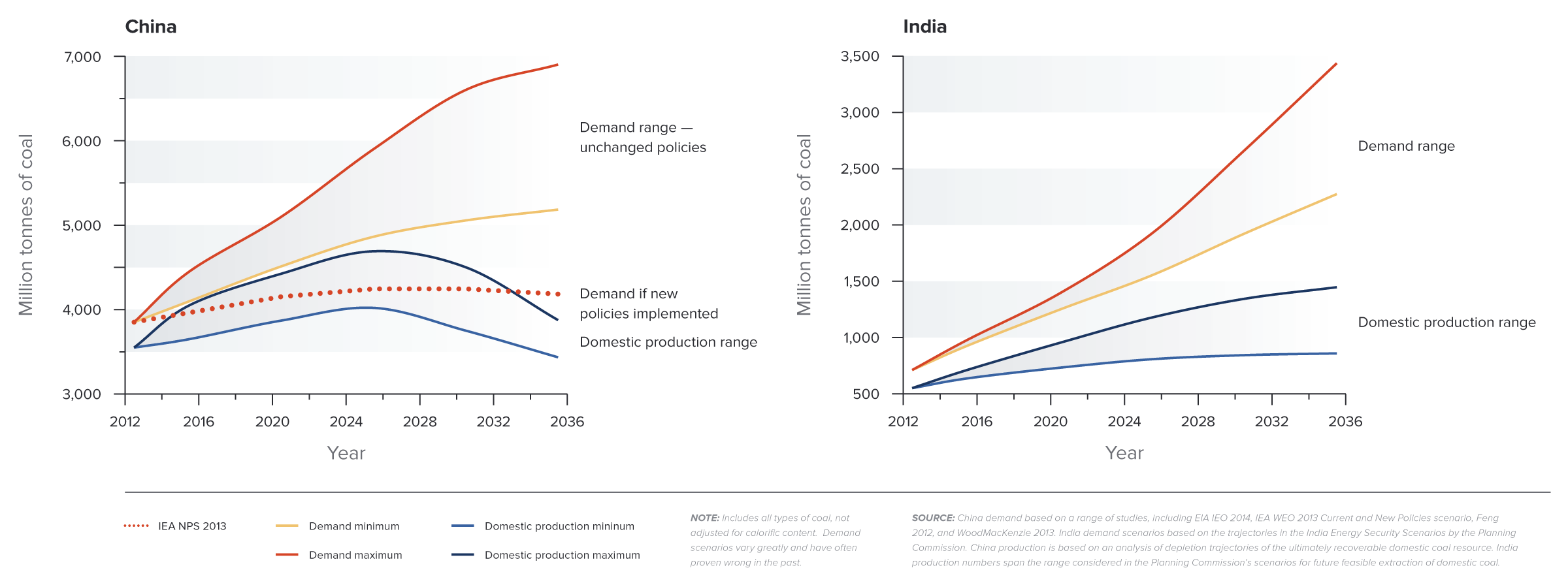

Coal has been abundant and affordable for many generations, and in several fast-growing economies, it remains the default option for rapid expansion of the power supply and for heavy industry. But conditions are changing, driven by fast-rising demand and a sharp increase in coal trade. Prices are twice the levels that prevailed historically,138 with projections for continued high levels in the range of US$85–140 per tonne, even as other options, notably shale gas in the US and renewable energy sources globally, have fallen in cost. The future security advantage of coal is also less clear than before. India has imported more than 50% of new coal requirements in recent years, and may face still higher import dependence without a change of course. 139

Note: Main ranges for demand scenarios do not assume policy changes to encourage steps towards lower coal use (China) or are based on a range of different energy efficiency developments for a given rate of economic growth (India). The broken line for China (IEA 2013, New Policies Scenario) illustrates a possible demand trajectory based on Chinese policies to curb coal demand growth. The figure includes all types of coal, not adjusted for calorific content.

Sources: China demand (non-broken lines) based on the range spanned by US Energy Information Administration, 2013; IEA, 2013, Current Policies scenario; Feng, 2012; and Wood MacKenzie, 2013. India demand scenarios are based on the trajectories in the India Energy Security Scenarios (IESS) in Planning Commission, 2013. China production is based on an analysis of depletion trajectories of the ultimately recoverable domestic coal resource. India production numbers span the range considered in the Planning Commission’s IESS for future feasible extraction of domestic coal. 140

The damage from air pollution has proven substantial and hard to address once coal-based infrastructure is built out; in China, mortality from air pollution is now valued at 10% of GDP. 141 In many countries, properly accounting for the cost of pollution erodes the cost advantage of coal. For example, coal-fired power has a financial advantage in much of Southeast Asia, at costs of US$60–70 per MWh. But properly accounting for air pollution can add a cost of US$40/MWh or more, enough to bridge or exceed the cost gap to alternatives. 142